PROSPECTIVE EMPIRICAL ANALYSIS OF KEY MACROECONOMIC INDICATORS AND RISKS

Emil Kalchev, PhD

New Bulgarian University, Department of Economics

Pro-European and pro-Atlantic government coalition was formed in Bulgaria in 2014. It inherited grave budget deficit, which was covered by a large portion new public debt. All ruling parties gain improved results in the municipal elections in October 2015, therefore they have incentives to further support the government. External political environment is rather very unstable and risky: surrounding military conflicts, refugees’ wave, etc. Profiting from the better economic conditions (weaker euro, low oil prices, cheap money, available EU funds and subidies), despite the precarious external environment, real GDP grew faster than anticipated (real 3.0% in 2015 and Q1 2016) amidst deflation environment. Main growth drivers were net export and increasing household consumption on the back of declining interest rates. Despite large gross budget deficits investments remained sluggish. Banking sector in overcame the turmoil around Corporate Commercial Bank and First Investment Bank as well the financial crisis in Greece.The quakes in the banking system remained isolated cases and did not affect the stability of the sector and the currency board. The main challenge for the banking industry in 2016 seems to be the Asset Quality Review and stress-testing. On the other hand, drivers of the economic growth are changing: external demand is weakening, whereas internal demand (household consumption in particular) is getting stronger. Against this backdrop, the trend of increasing public indebtedness is risky, as many negative examples for the long term consequences of such tendency exist.

Keywords: Applied Macroeconomics, Internal and External Economic Environment

1. Political Environment

The GERB dominated government formed in Bulgaria in 2014 inherited grave economic problems: revoked license of the fourth-largest Corporate Commercial Bank (CCB), envisaged state budget deficit for 2014 beyond the Maastricht threshold of 3.0%, deficit of the National Electricity Company of EUR 1.6 bn, frozen EU Operative Programmes, etc. The most socially explosive issue, however, was the CCB case: the bank has at that time negative capital of EUR 1.9 bn (around 5.0% of the GDP).

Currently, approximately 2 years later, internal political situation seems to be relatively stable, despite the lack of complete coherence in the ruling coalition and particular coalition members, as the Reformist Block, since GERB dominated political setting has no real alternative in the middle term. Against the background of growing economy, politically initiated structural reforms in judiciary, healthcare and education faced delays and obstacles, leading recently to changes of ministers (education and justice).

Within the judicial reform, at the end of 2015, the Parliament adopted the bill amending and supplementing the Constitution of the Republic of Bulgaria. By the envisaged changes, the Parliament will be able to hear and approve reports of the Prosecutor General concerning activities of the prosecution. The amendments foresee the division of the Supreme Judicial Council (SJC) into two colleges – one of judges and another of prosecutors. College of Judges will consist of 14 members, including the chairmen of the Supreme Court of Cassation (SCC) and the Supreme Administrative Court. Six members will be directly elected by judges and six by parliament. Prosecution College shall consist of 11 members, including the Prosecutor General, four members elected directly by prosecutors, a member of investigators and five of the National Assembly. Supreme Judicial Council in turn will be able to exercise its powers through plenum of judicial and prosecutorial staff. SJC members from the parliamentary quota will be elected by a majority of two thirds of the deputies. Between the first and second readings, the texts were amended, which led to some tensions within the coalition government and the resignation of the Minister of Justice.

The annual report of the European Commission to the European Parliament and the European Council on the Progress in Bulgaria under the Co-operation and Verification (CVM) Mechanism from January 2016 stated, however, that the progress regarding the judicial reform and the tackling of corruption and organized crime is slow. According to the report, it is necessary to show that the judicial reform is a political priority by taking concrete practical steps towards its implementation. The public scepticism in this area is fuelled by insufficient action taken by the authorities regarding the transparency and the reforms in the judicial system, as well as corruption in the top levels, and the lack of adequate prosecution towards it.[1]

Moreover, the vice prime minister responsible for social policy resigned for political reasons, despite more or less successful conducted pension reform, [1] creating short-term vulnerability in the coalition, which, however, remained stable. Otherwise, the second strongest opposition party, the Movement for Rights and Freedoms, plunged into a harsh leadership crisis in December 2015 due to different position on Bulgaria - Turkey foreign relations.

The presidential elections in autumn 2016 are definitely the most significant political event for the year that is shaping the political environment. Furthermore, they are considered as an indicator for the alterations in the electoral attitudes and thus for predictor for the possible outcome of the next parliamentary elections. As long as parties refrain from early public nominations for the time being, most likely, the vote will be decided at the last moment, driven more by emotions of the voters.

Generally, the political will to conduct needed structural reforms in the juridical system, as well in the pension, healthcare, energy, transport and education sectors turned out to be weak. Therefore, until the end of the mandate of the government efficient structural reforms are not expected.

Against the background of the rather stable internal political situation, despite some potential budding party frictions within the ruling coalition, external risks appear more unpredictable and far-reaching (military conflicts, ISIS, refugees, terror attacks in the neighboring region, Grexit, Brexit, refugees flood, etc.). In particular, the flow of refugees, striving to Western Europe, partly passes through Bulgaria, which, however, is not their end destination. Although the mid-term development of this problem is difficult to predict, it is a huge potential foreign risk to the country. All in all, balancing in a harder global confrontation, Bulgaria has to remain a true partner in NATO and the EU as this foreign policy orientation has clearly no alternative. In this regard, the challenges are to diversify the nearly total dependency on Russia in the energy sector and to balance the foreign political orientation towards neighboring countries (incl. Turkey).

In April 2016, Bulgaria presented revised National Reform Program and Convergence Program. The EU Council, after analysing both documents, recommended the country to take action in 2016 and 2017 to:

1. Achieve an annual fiscal adjustment of 0.5% of GDP. Further improve tax collection, take measures to reduce the extent of the informal economy, including undeclared work.

2. By the end of 2016, finalise the asset quality review and stress test of the banks, complete the balance-sheet review and stress test of the insurance companies and the review of private pension funds' assets.

3. Reinforce and integrate social services and active labour market policies. Increase the provision of quality education for Roma and improve the efficiency of the health system. Increase the coverage and adequacy of the minimum income scheme.

4. Reform the insolvency framework and increase the capacity of the courts regarding insolvency procedures. Strengthen the capacity of the Public Procurement Agency, including speed up the introduction of e-procurement.[2]

Not only these recommendations address the key issues in political-economic area, but also, they have to be followed by the government. Hence, they are good indicators for the future policy measures expected in the economic environment.

Although GERB will expectedly receive the most of the votes in next parliamentary elections, most likely they will not be able to achieve a majority. Thus, they will have to manage a next coalition in a changing political situation: significant parties’ fragmentation in the background of a low coalition culture. The ongoing fragmentation is not only a consequence of the discontent with the politicians and the widespread corruption in public life, but also a result of the incapability of the bigger political parties to reform in a positive direction. On the other hand, covered problems in judiciary, public finance, energy sectors, healthcare, and education require a stable and effective majority in the Parliament. A lack of compromise, willingness and unsuccessful negotiations can lead to further new elections and chronic instability.

The political setting, fuelled by the presidential elections in autumn, is not expected to hinder or stimulate economic trends, against the backdrop of sluggish structural reforms and some potential political frictions in the coalition. External political environment, however, will remain as source of potential social and economic instability (military conflicts, refugees’ wave, etc.).

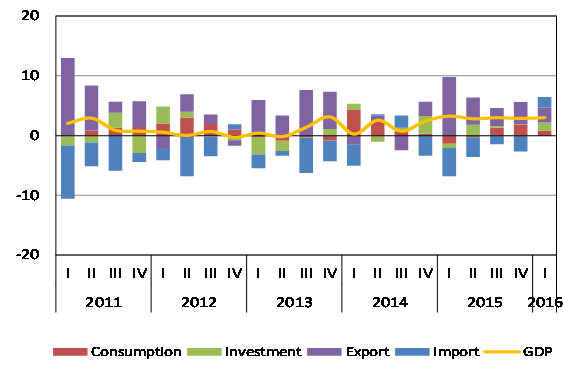

2. Recent Dynamics and Short-Term Outlook of GDP

Gross domestic product (GDP), an indicator of the dynamics of the national economy, is composed on the demand side of consumption, investment and net exports. On the other hand, investment and consumption (including imports) define domestic demand, while net export - external demand. Both determine the aggregate demand that drives the GDP dynamics.

The research of the contributions of these elements to the GDP growth shows a clear cyclical development with one year frequency over a five-year retrospective period.

Table 1: Contributions to Real GDP Growth on the Demand Side (pp)

|

| 2011 | 2012 | 2013 | 2014 | 2015 | Q1 2016 |

|

| Real GDP growth (%) | 1.6 | 0.2 | 1.3 | 1.5 | 3.0 | 3.0 |

|

| Contribution of internal demand(рp)

| 0.2 | 2.5 | -1.3 | 2.7 | 0.9 |

2.2 |

|

| Contribution of internal demand(рp)

| 1.4 | -2.3 | 2.6 | -1.1 | 2.1 |

0.8 |

|

Source: National Statistical Institute, Own Calculations

Thus, the contribution of domestic demand was decisive for the real GDP growth in 2012 and 2014, while, conversely, mainly external demand supported the growth in 2011, 2013 and 2015. Following this model, domestic demand should be again the main engine of growth in 2016.

In particular, in 2015, real GDP grew by 3.0%, improving significantly the result from 2014 (1.5%). On the demand side, one of the main contributors for this positive dynamics was foreign demand (5pp), while domestic demand had a milder effect with 0.9pp. Final consumption was leading factor on the side of domestic demand, contributing 0.5pp to the GDP growth, followed by gross capital formation with 0.4pp, as import had an effect in the opposite direction (with -2.9pp).

Graph 1: Contributions to Real GDP Growth on the Demand Side (pp)

Source: National Statistical Institute, Own Calculations

The growth of the final consumption was a result of increased individual consumption out of which the biggest contribution to the growth of GDP had household consumption (0.5pp). The latter was driven not only by the increase in the two components of income in the framework of the Gross Value Added (GVA), but also by the lowering of the interest rates in the country.

Thus, in 2015 households spent 0.8% more than in the previous year. Within the components of income, compensation of employees grew faster (2.8% yoy in nominal terms) than the gross operating surplus (0.2% yoy), primarily due to measures for increase of salaries, rather than improved financial performance of companies in the economy.

Indeed, unlike all quarters of 2015, the positive influence of external demand on the economic growth in Q1 2016 became weaker. As a result, net export contributed 0.7pp for the dynamics of the GDP, which increased by 3.0% yoy in real terms. When it comes to the internal demand, the positive impact to the growth of the economy was given by the household consumption (2.0pp) as well as net investments (1.4pp).

In nominal GDP terms the compensation of the employed working force grew by 10.6% yoy in Q1. In this context the gross operating surplus, which is an indicator for firms’ production activities, continued decreasing by 0.8% (-5.9% yoy in Q4 2015).

In line with the positive growth environment in Central and Eastern Europe, GDP of Bulgaria grew in Q1 2016 faster than expected, repeating the result of 2015. Otherwise, not only external demand, but also much stronger domestic one were GDP drivers. Based on rapidly growing average salaries (8.3% yoy) and low interest rates on deposits (avg. 0.7% p.a.), household consumption soared, supporting stronger the GDP growth, while gross fixed capital formation contributed moderately. Accordingly, net export contribution narrowed.

This new private consumption-driven growth model is anticipated to sustain further in Q3 and Q4 2016, following the ongoing common pattern for the CEE region. In fact, it could be considered as a result from the ECB’s QE policy, which in addition will push inflation into positive territory in H2 (0% as of May 2016). Against the background of flourishing private consumption, export and investments are expected to become more sluggish than in 2015. In this respect, doubts about the middle term competitiveness of the national export might not be groundless, as sustainable export acceleration can also not be statistically observed. On the other hand, weaker EU funding in 2016 due to new EU programming transition period will limit public investments, which will not be substantially compensated by the state budget. Furthermore, narrowing year on year lending to businesses since end-2014 in declining interest environment (avg. 5.5% p.a. in Q1 2016), along with double digit increase in corporate deposits since November 2015 clearly point out insufficient investment opportunities for private non-financial enterprises. In addition, inquiry of the National Statistical Institute estimated 4.2% yoy decrease of private investment in industry in 2016.[3]

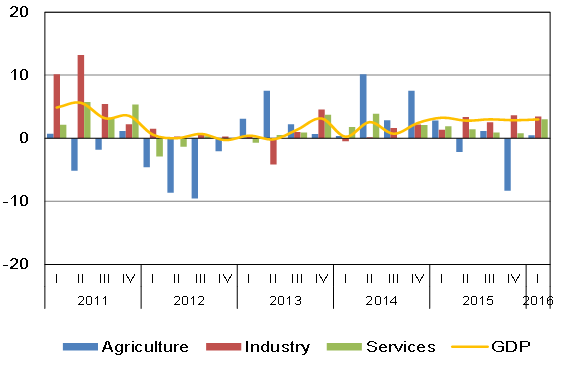

On the supply side, positive contribution to the growth of GDP had not only the services (0.7pp) but also the industry (0.7pp) in 2015, while agriculture registered a negative contribution of -0.1pp. [2]

This structure of contributions promises an improvement taking into account the structure of GVA of the Bulgarian economy. In it, services took 67.2% relative share, industry 27.6% and agriculture 5.1% for 2015. The fact that the services and the industry had an equal contribution to growth reflects an improvement in the industry sector, which holds the best potential for long term growth.

Graph 2: Contributions to Real GDP Growth on the Supply Side (pp)

Source: National Statistical Institute, own calculations

In Q1 2016, solid contribution to the GDP growth came from services (1.8pp), followed by industry (0.8pp), while the agriculture remained flat (0.0pp). In the services sector, as expected, trade and repair of motor vehicles, hotels and restaurants (0.7pp) and operations with real estate shore up the growth most intensively. They were followed by the financial and insurance activities (0.2pp.), scientific research (0.2pp.), creation and dissemination of information (0.2pp), etc. These facts reflect what happened in the sector in Q1 2016: purchases of motor vehicles and real estate due to considerable available consumer savings and drop of loans and deposits interest rates.

For the entire 2016 a real GDP growth between 2.5 and 2.9% is considered, driven mainly by household consumption and to a lesser degree by the investments, which will be reduced due to weaker EU funds absorption. [3] The consumption will be supported by growing salaries and lower interest rates on deposits and loans. On the production side, efforts of the economic policy should be aimed at creating conditions leading to a permanent increase of the industry share in GDP.

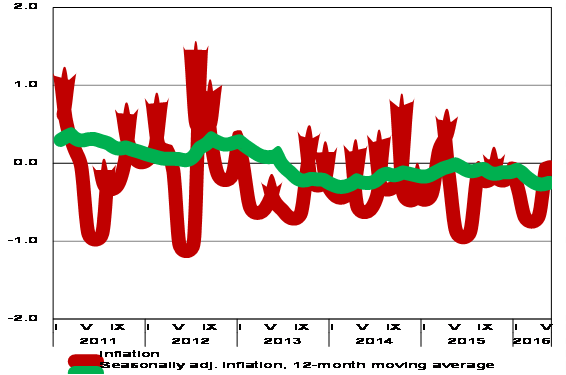

3. Inflation and Unemployment Rates

After 2014, 2015 was also as a year of deflation. The average annual inflation contracted to -0.1%, while December to December inflation was -0.4%. During 2015 prices of transport and healthcare dropped, while food, hotels and restaurants exhibited increases.

Graph 3: Consumer Price Dynamics (%)

Source: National Statistical Institute

Monthly inflation for May 2016 stood at 0.0%, indicating an anticipated reversal of the deflationary trend in 2016.

This trend reflects the ongoing ECB’s QE policy and the most likely development of the electricity prices. They are envisaged to be raised, due to the huge deficits in the energy sector.

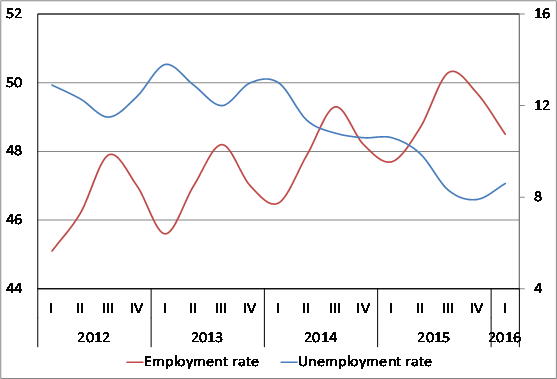

The unemployment rate at the end of 2015 was 7.9% (2.7pp lower than the level of the previous years’ end). In turn, the employment rate increased by 1.5pp to 49.7%. The average monthly wage rose during the year by BGN 66 to BGN 955 from BGN 889 at year-end 2014.

Reflecting the positive dynamics of the GDP in Q1 2016, the employment rate rose by 0.8pp yoy to a level at 48.5%.

Graph 4: Employment and Unemployment Rates (%)

Source: National Statistical Institute

Otherwise, the unemployment rate decreased by 2.0pp to 8.6% in Q1, which usually is the highest quarter rate in the year. Thus, in Q3 and Q4 2016 unemployment rate is forecast to continue declining moderately below 8.0% eop.

The wage increase in the public sector was BGN 75 and in the private sector BGN 45 in 2015. Thus the private sector wage reached BGN 937, still substantially lower than the public sector average of BGN 1012.

4. Rediscovering the Magic of Pubic Debt

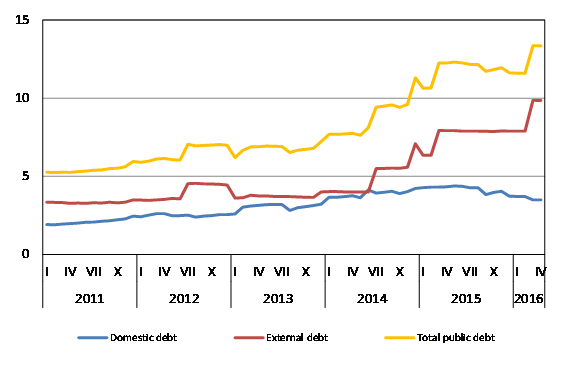

To cover the inherited budget deficit for 2014 the new coalition issued government bonds of BGN 1.6 bn in the domestic market and borrowed additionally EUR 1.5 bn from four international banks. Due to the low interest rates in the Eurozone, the international financial market, however, became the main source for financing the budget deficit. So,on 19th March 2015 Bulgaria tapped the international markets and raised a record EUR 3.1 bn under newly established EUR 8 bn Medium Term Note (MTN) Program. The deal has been met with sound interest by a vast list of investors, eager to capitalise on the overall macroeconomic stability of the country and its relatively low debt-to-GDP ratio. Bulgaria has closed the deal, printing 3 fixed rate tranches (7-, 12-, 20-year) at low levels (coupons 2.0%, 2.625%, and 3.125%, respectively). Parliament debates earlier this year have questioned the need of a MTN and coalition partners were not unified initially in their support. However, this has not proved detrimental to proceeding further. The transaction has almost utilised in full the state budget limit for 2015. [4] Part of the deal proceeds were meant for repayment of the EUR 1.5 bn bridge-to-bond loan, drawn in 2014. In their annual visit to Bulgaria, IMF have outlined that "...deterioration in the fiscal balance has tested Bulgaria’s hard-won macroeconomic and financial stability" and pointed that the country needs "a structural balance by 2019".[4]

On the 14th of March 2016 Bulgaria tapped again international markets and raised EUR 1.994 bn under the 2015 EUR 8 bn Medium Term Notes (MTN) Program. The offering was “successful”, as total demand amounted to EUR 3.6 bn, nearly two times higher than the amount tendered. Investors were drawn by the macroeconomic stability of the country and the deal’s attractive conditions. Two fixed rate tranches were printed – a 7, and 12-year bonds – at record low levels (with coupons of 1.875% and 3.0%, respectively). The 2016 transaction is expected to increase Bulgaria’s debt-to-GDP ratio up to 30.3% from 26.4% as of yaer’s end 2015. Proceeds are intended to be used as a fiscal buffer for the banking system. Despite Bulgaria’s low debt levels relative to most countries in the Eurozone, a number of structural issues have been addressed by international institutions including a weak judicial system. No new issuance is expected under the program before 2017 as the State Budget Law caps the total international issuance for 2016 at EUR 2.0 bn.

Aiming at restrictions loosening for going into more public debt, amendments to the Low on Public Finance were proposed. They were believed to be motivated by the discussion in the EU for introduction of flexibility in the application of rules for fiscal and economic governance. In turn, the changes are associated with easing of government’s fiscal discipline and tightening the financial control over municipalities. For example, the requirement that the cash budget deficit have not to exceed 2.0% of GDP will be abolished. Anyway, in practice this rule has not been applied in the last two years. Furthermore, under certain conditions (such as "major investment projects") a larger structural deficit can be acceptable. Whether a project is so important that it triggers changes in the structural deficit rules is clearly a matter of justification. However, there is no intend taxpayers to be asked whether this justification is persuasive for them or not.

Graph 4: Internal and External Public Debt (EUR, bn)

Source: National Statistical Institute

Changes related to the municipal finance provide for the right of the Minister of Finance to manage municipalities in financial difficulties, in order to be provided with interest-free loans, which is a measure of vague political legitimacy and unpredictable consequences in practice.

At end of 2015 public debt amounted to BGN 22.7 bn or 26.4% of GDP, one of the lowest in the EU. As of April, it rose by BGN 2.1 bn or by 8.9% yoy, which amounted to 29.2% of GDP.

Along with intensifying international public debt issuance Ministry of Finance proposed a reform of the second pillar of the pension system. The draft sets out second pensions from private pension funds to remain life-long, but they will be paid from a common pool instead of individual accounts. Monthly contributions and returns will be accrued on individual accounts, but they will enter into the common pool, after pension rights are acquired. It will support the longevity risk sharing between insured individuals, thus ensuring the life-long nature of the pension and its size. However, in case of death of the pensioner, the remaining amount of the pension will not be paid to his heirs. Further, pension funds will have more opportunities for investment in terms of a broader range of financial instruments, inclusive investments in bonds of international financial institutions. However, the possibility of an investment in real estate is excluded due to the difficulty of making a fair assessment of the real estate.

As a whole, government's increasing financing needs could be a source of risk. Although still low compared to EU peers. Debt servicing has not been significantly affected because of the favourable financing conditions presented by the low-interest-rate environment in the last few years. However, the situation could change in the medium term. An additional risk factor is the growing size of contingent liabilities related to the state-owned enterprises, most notably in energy and transportation sector.[5]

The Parliament approved taking out of two new loans amounting to a total of BGN 1.2 bn in June 2016, which will be provided for the needs of the Deposit Insurance Fund (DIF). Loans will be issued by the International Bank for Reconstruction and Development and the European Bank for Reconstruction and Development. They will be activated in case of “need” which means that if DIF does not need these resources, they, in reality, will not be absorbed and no interests will be paid.

Loans from both financial institutions will amount to BGN 600 mn each. They will be used to fill the reserves of the fund and it will support the optimization of its financing structure. The reserve was significantly depleted after the insolvency of Corporate Commercial Bank (CCB) in 2014 when the fund had to repay the insured deposits at CCB.

5. Lesions on Internal Risks from the Near Past

Frozen EU Funds

In 2014, the European Commission (EC) suspended payments to Bulgaria on Operational Program (OP) Regional Development as a result of an audit, which found out problems in the management and control of the European funds. OP Environment had been the first program with suspended payments at the end of 2013. Decision had to be made whether the payments on OP Environment to be restored or permanently shut down. The particular reason EC to impose sanctions on the OP Regional Development was many violations of the EU rules regulating public procurements. The payments were suspended until the government took necessary measures to correct the irregularities. The government had to disburse money from the national budget in order to cover the lack in the EU funds. The problems of the OP Regional Development coincided with infringement procedure over the South Stream gas pipeline opened by the EC. This puts further the implementation of the state budget at risk.

The Corporate Commercial Bank Case

On 21 June 2014, the Bulgarian National Bank (BNB) received an official letter from Corporate Commercial Bank (CCB), the fourth largest bank in Bulgaria, in which CCB announces suspension of all payments and other bank transactions. The BNB acted immediately putting CCB under special supervision and appointed conservators. The trade of CCB shares on the Bulgarian Stock Exchange was suspended. Later, the subsidiary of CCB Credit Agricole Bulgaria was also placed under special supervision. It was taken the decision that the government and the BNB had to secure the needed liquidity of CCB, as funds had be provided by the Bulgarian Bank for Development (BBD) and the Deposit Guarantee Fund (DGF). The shareholders’ capital of the two banks had to be written off and their rights forfeited. As a next step a capital increase was envisaged, as BBD and DGF had to be in charge of it. These steps of reorganization had to be completed by 20 July 2014. On 21 July the banks had to start their normal activity.

The BNB changed, however, its initial plan to reopen for clients the Corporate Commercial Bank and its subsidiary Credit Agricole Bulgaria on 21 July and decided to prolong its special supervision up to 23 September. Independent auditors of the banking group had found out a lack of essential parts of CCB’s credit records related to a credit portfolio in the amount of EUR 1.8 bn (out of EUR 2.8 bn total portfolio). Moreover, this credit portfolio showed a strong link between the debtors and the major shareholder of CCB. A conservators’ separate audit revealed that an amount of EUR 105.3 mn was systematically withdrawn on behalf of the major shareholder.

Due to suspected criminal acts the case was given to the Prosecutor’s Office. The BNB in turn, decided not to nationalize the CCB, due to concerns about affecting the function of the Bulgarian Development Bank and other public lenders. Instead, BNB offered to nationalize the “healthy” Credit Agricole Bulgaria EAD, transferring all “good” assets and liabilities of CCB to its balance sheet. As a solvent state-owned bank it had to be further financially supported by the Deposit Insurance Fund, the State budget, and the BNB. Moreover, all citizens’ and firms’ deposits had to be fully guaranteed, excluding only those connected with the majority shareholder. Finally, the license of CCB had to be revoked and all depositors to be paid in full. This plan, however, could be fulfilled only if a special law was adopted. Nevertheless, this part of the BNB’s was not accepted by the leading parliamentary parties. Of course, such a law would definitely calm down the situation around banks, but this would have had a negative impact, driving other banks on bearing unreasonably higher risks. Furthermore, all big CCB depositors had been well known about the deposits’ guarantee limit according Bulgarian law. Despite that they consciously placed their money in the CCB on higher interest rates than in other banks.

Meanwhile, the negative news flow and the special supervision for CCB have driven down the value of its publicly-traded corporate bonds, listed in Dublin, Ireland, which were taken off the exchange. The bonds, a dollar issue with a nominal value of USD 150 mn, were due 8 August. The issuer has missed the repayment of the principal and the accrued interest with the value of the bonds.

On 22 October the BNB published a summary of the long-awaited audit report, prepared by Deloitte Bulgaria, AFA, and Ernst & Young Audit on the state of CCB. It showed the necessity of loans’ impairment of BGN 4.2 bn (total assets of BGN 6.7 bn). Also the capital of CCB dropped to BGN 198 mn (BGN 521 mn as of June).

On 30 October the BNB received a letter of intent of the State General Reserve Fund of Oman (SGRF), Gemcorp Capital LLP (GemCorp) and EPIC Group (EPIC), which had formed a consortium. The consortium offered the Bulgarian Government to provide BGN 2.3 bn as a cash capital contribution for stabilizing the CCB. Simultaneously, the consortium would provide the required top up in assets and cash to CCB to fill the agreed shortfall (it is to be agreed additionally on the base of the auditors’ report). Guaranteed depositors wishing to withdraw would be paid in full without the activation of the depositors’ insurance scheme. The non-guaranteed depositors may need to accept a haircut as part of the bail-in of the existing creditors, and certain depositors of the CCB. They will be given an incentive to keep their deposits with the bank for a longer time period. Those depositors who elect immediate withdrawal of their deposits will receive payment (less haircut) in the form of Bulgarian Government bonds.

On 31 October the new Bulgarian Parliament was debated on the proposal of the consortium. First, the parliamentary parties were willing to restructure the CCB. After the presentation of the letter of intent of the consortium - in particular, the expected support of the Bulgarian Government of BGN 2.3 bn and the not clear history of some participants in the consortium - the Members of the Parliament decided not to accept the proposal and to liquidate the CCB.

Because the capital of CCB will become highly negative due to the huge loan impairment, the BNB revoked the license of CCB on 6 November and started a bankruptcy procedure.

In connection with the CCB case and financial difficulties with the National Health Insurance Fund (NHIF), amendments in the State Budget Law for 2014 were proposed by the Council of Ministers. They were motivated by the need of strengthening the financial stability in the country. In first place, the amendments foresaw an increase in the public deficit by EUR 1.7 bn, which had to make possible actions, securing the economy and the stability of the financial system (EUR 1.4 bn for bank stabilization, BGN 370 mn for State budget support). Moreover, state guarantees in favor of the Deposit Insurance Fund had to be enhanced by up to EUR 1 bn. The State budget deficit had to be increased by EUR 370 mn (by 0.9% of the forecasted GDP).

Banking sector as a whole underwent financial strain, as a run on the fourth largest Corporate Commercial Bank (CCB) and its subsidiary Commercial Bank Viktoria (CBV) caused a massive deposit withdrawal in June. Due to liquidity depletion the Bulgarian National Bank (BNB) put both banks under special supervision. Only for a week the liquidity pressure spilled over to other credit institutions and in particular to the third largest First Investment Bank (FIB). FIB was saved on account of EC approved government support; CBV opened doors, whereas CCB was practically liquidated by the end of the year. In November, CCB was excluded from the BNB’s supervisory statistics, which affected the data on the sector: total bank assets shrank by 0.7% yoy to BGN 81.5 bn as of December (Dec’2013: BGN 85.7 bn). The liquidity crisis in the CCB and FIB remains isolated case as there were no signs of similar problems with other Bulgarian banks. Moreover, the interbank overnight lending rate underwent no significant changes. From current point of view this case could not threaten the stability of the currency board.

Nevertheless, three months before the end of his term BNB’s governor Ivan Iskrov announced his resignation on 10 of July 2015, which was long awaited and welcomed by political parties and financial markets, as during Iskrov’s mandate the fourth largest Corporate Commercial Bank collapsed.

The failure of CCB shed light on serious weaknesses in the banking sector supervision, on the inadequate actions of the national institutions and the BNB in particular. The time frame stated in the law for the election of a successor was 10 July-10 August, who had to take office on 10 October 2015. Central bank governor is appointed by the Parliament and his mandate is of six-year term. However, Iskrov requested the new elected governor to take office on the 10 of July. The new governor was expected to restore in the shortest time the trust in Bulgaria's banking sector and banking supervision, which was shattered during the governance of Iskrov. He also had to take measures to reduce the spillover effects of an eventual Greek default over the Bulgarian banking sector and to appoint a new deputy central bank governor in charge of the banking supervision, as this position had been vacant for months.

A senior economist with the International Monetary Fund, Dimitar Radev was elected for the position of governor of the BNB. He had a twenty-one-year long career in the Ministry of Finance and had been a deputy minister of finance in two governments in the end of the 90's. Afterwards, for fourteen years he had been working with the IMF, where he is involved in providing technical help for countries in financial crisis.

As a result of the CCB’s failure not only personal changes were initiated but also the low was amended. So, the Parliament adopted an entirely new Law on Deposit Insurance in Banks. According to it, the Deposit Insurance Fund (DIF) sets annual premium for each bank, taking into account its risk profile and the amount of guaranteed deposits in the bank for the previous year. The new text of the law expands the scope of insured deposits since some groups of non-guaranteed deposits under the repealed act were dropped. The guaranteed amount remains at BGN 196 thousands; however an exception is introduced for certain category of deposits for which the amount is BGN 250 thousands. The period in which the DIF is obliged to start paying back insured deposits is significantly shortened from 20 days under the repealed act to 7 days under the new one. The DIF is obliged to carry out regular stress tests to the system of deposit insurance as well as to banks when information for problems, which could lead to activation of the scheme for deposit insurance, is presented from the BNB.

Energy Sector – Ticking Time Bomb

High fiscal risk in the middle term for the fiscal sector arises from the alleged National Electric Company’s deficit. It could be either covered by politically very unpopular price increase, or simply be nationalised. The 2013 financial results of the Bulgarian Energy Holding (BEH) were marked by weaker operating profitability in all major segments, an increased loss from discontinued operations, and negative free cash flow (due to the slide in operating cash flow). Moreover, the company`s situation is further aggravated by the legal disputes related to the decision to halt construction of the Belene nuclear power plant, as well as the company’s inability to make reasonable estimates of losses and a failure to recognize sufficient provisions. In terms of contingent liabilities, the group has entered into legal proceedings against Atomstroyexport. Another negative fact was the suspension of construction of the South Stream gas pipeline. When Corporate Commercial Bank was placed under special supervision on 20 June 2014, the account balances of BEH with the bank accounted for less than 25% of the company’s total cash. However, this had not a short term impact on Bulgarian Energy Holding’s liquidity, as the company’s cash reserves comfortably covered its short-term debt.

Currently, BEH and his advisers began a series of meetings with investors in securities with fixed income in the UK and continental Europe. BEH is expected to offer medium-term fixed income financial instruments. The bonds will be listed on the Irish Stock Exchange, where it was placed first bond issue of BEH in 2013. The aim of BEH is to issue bonds amounting to EUR 500 mn, which should cover the bridge loan of EUR 535 mn that BEH got in April 2016 by the consortium of international banks.

Uncertain Internal Economic Environment

Generally, internal economic environment seems to be rather problematic, as business survey of the National Statistical Institute among the sectors of the economy showed. Concerning the industry, the forecasts are less favorable as a consequence of the uncertain economic environment. Meanwhile, a stronger negative impact of the factor ‘weakness in economic legislation’ is observed, which shifts to the third place the factor ‘insufficient domestic demand’. The assessment of the construction entrepreneurs is positive, indicating stable construction activity. Obstacles for the sector’s development, beside the uncertain economic environment, are the competition in the branch and financial problems. In turn, retailers have more optimistic assessments about the present business situation. They also expect an increased volume of sales over the next months. As the main factor limiting the activity in the branch retailers point out the insufficient demand. On the other hand, the indicator for the business climate in service sector remains unchanged. The tendency for services demand is estimated as decreasing and the expectations over the next three months are also more reserved. Again the uncertain economic environment remains the most serious obstacle for the business, followed by the competition in the branch and the insufficient demand.[6]

6. External Risks – Unpredictable and Fare-reaching

Russia-Ukraine

The conflict between Russia and Ukraine raises great concern, possessing the issue of Bulgaria’s economic dependence on these countries. Generally, Bulgaria relies on energy imports, which accounts for 23% of the total imports. In this regard, almost 2/3 of the imported energy resources come from Russia and Ukraine, which indicates for extremely high economic dependence. The fact that visitors from Russia and Ukraine total 25% of foreigners’ overnight stays in Bulgarian tourist industry further increases the dependence on the conflict between the two European countries. In terms of FDI, 25% of them came from Russia in 2012 and 7% in 2014.

“Grexit”

Financial strain in neighboring Greece in 2015 was potential external risk factor for the Bulgarian Banking sector as share of Greek banks in bank total assets was around 16%, slightly shrinking on an annual base. United Bulgarian Bank, Piraeus Bank and Alpha Bank were 100% owned by Greek parent banks. Although their capital Greek-ownedthese banks fall under Bulgarian regulations, which isolates them from the immediate influence of what is happening in Greece. Otherwise, a portion of the capital outflow from the Greek banks came into the Bulgarian banking sector, which remained stable.

The key monetary indicators showed that the four Greek/Greek-owned banks were stable. No significant changes in the statistics could be identified. BNB took steps to support the liquidity of the Greek subsidiaries such as mandating higher deposits with the BNB, requiring higher proportion of liquid assets held and reduction of the exposure to parent banks. Otherwise, no behavioral tensions for runs on the Greek subsidiaries could be identified. Moreover, a process of deposits withdrawals from the Greek subsidiaries had been running, not causing any visible liquidity difficulties for these credit institutions.

The Bulgarian National Bank recommended banks with Greek capital to clean their exposures to Greece in order to limit the risk in case of worsening the relations between Greece and the EU. In general, there are four banks with Greek capital in Bulgaria: United Bulgarian Bank, Eurobank Bulgaria and Piraeus Bank Bulgaria, which are local companies, and Alpha Bank S.A., a branch of a Greek credit institution. In total, they held a share of 23.0% of the assets in the sector, as of end 2014. The three Bulgarian banks with Greek capital reported high capitalisation and liquidity. They are less at risk from the Greek side than Alpha Bank, as it primarily is subject to the Greek regulations, but not to Bulgarian ones. However, the BNB has tools to influence the Alpha Bank, in order to eliminate potential risks. Possible liquidity problems of the parent banks in Greece could create momentum for selling bank units in Bulgaria, which would accelerate the consolidation process in the sector.

Due to the situation in Greece the spread of Bulgarian 10 year T-bond widened by 20bp, which is lower than in other countries, e.g. Lithuania, Poland. Most likely, the current market valuations are not reflecting possible headline risks of the non-payment situation in Greece.

Greece was the fifth-biggest FDI investor in Bulgaria in 2015, which evolved compared with the same period last year when a net outflow of FDI was observed. In default case the FDI dynamics is ambiguous: Greek FDI could flow back to Greece due to better FX export conditions; Greek businesses could move to Bulgaria taking advantage of the more stable and solvent business environment.

Although Greece is among the top 10 trading partners of Bulgaria, a lot of adjustment has already taken place in the recent years to lower the risk of exposure of the international trade. As of 2015, the share of the export to Greece was 6.4% of the total export, while the import accounted for 4.1% share.

All in all, the main channels of potential impact from the financial strain in Greece: banking sector, capital markets, FDI, international trade, showed a limited potential to negative effects on Bulgarian banking sector and economy. It turned out that expected negative effects on the banking sector and the economy by the financial tensions inGreece must have been overestimated. In particular, Greek-owned banks maintain high capital adequacy and are highly independent on financing from parent banks and the Greek state.

Brexit

On 23 June 2016, UК decided to leave EU. In order to assess the impact of this decision on the Bulgarian economy, it should be taken into account that 1.8-2.5% from the Bulgarian export goes to the UK, whereas the British import amounted to 1.6-2.0% of total import. Positive trade balance for Bulgaria is observed (0.15% of GDP for 2015), but the depreciation of the GBP against the BGN is likely to make it negative. On the other hand, British FDIs, between 2009 and 2015 are negative (-3.0% of total FDIs) and the process of disinvestments is expected to accelerate. It is obvious that Bulgaria does not heavily depend on British trade and FDIs. Moreover, British financial institutions are not largely presented in the Bulgarian financial sector. Therefore, no direct impact also on this sector is envisaged. However, through international parent companies and international financial markets indirect impact on Bulgarian economy seems to be more likely. Additionally, due to Brexit, Bulgaria could lose around 5% of the total subsidies, according to budget frame of the EU (approx. EUR 550mn for the next 7 years). Additionally, Bulgarian contribution to the EU budget may increase. The appreciation of the BGN could create incentives of selling British properties in Bulgaria, and discourage new purchases. Having in mind the strong demand for Bulgarian properties in 2015 and the appreciation of the other EU currencies, it could be the case that the demand will intensify.

All in all, the negative and positive effects of Brexit could hardly be weighted; since it is even not excluded that Bulgaria could be a net winner from it, after possible short term negative effects on the international trade and Bulgarian emigrants.

7. Banking – the Most Sensible Sector?

Generally, the tide economic environment hinders the growth and the profitability perspectives of the banking sector, making it not quite attractive for bank deals. Otherwise, the once fourth largest Corporate Commercial Bank closed doors last year, freeing up market space for other banks. Moreover, despite this strain the total profit of the sectorrose in 2014, promising a further growth. Since 2009, when the global financial crises reached Bulgaria, a strong consolidation process was expected, which, however, has beenonly partially realized due to the fact that about 75% of the Bulgarian banks are foreign-owned subsidiaries of European credit institutions. Therefore, the consolidation process is determined rather by the parent institutions within their global strategies than merely by the economic environment and the ratability situation in the country. In this respect, if a consolidation between parent banks takes place, most likely, it will result in deals in Bulgaria.

Bolstered by the stable macroeconomic environment in the country in 2015, the banking sector in Bulgaria succeeded in strengthening the confidence in the system. The financial crisis in Greece had limited impact over the Bulgarian banking system and did not lead to systematic risk. Bulgarian banks had managed to accumulate high liquidity and capital buffers owing to their sound governance and the BNB’s focused conservative policy. At the year end the liquidity ratio, showing the ability of banks to repay their debts, further improved to 36.71%, compared to 30.12% a year earlier. The Central Bank implemented a series of regulatory and organizational changes and appointed the new Governor of the institution before the expiry of the mandate of his predecessor. Bulgarian banks continued to carry out daily activities as usual and managed to generate high profit in an environment of declining interest rates and increasing deposit base. The registered net profit of the banking system was BGN 898.43 mn which is BGN 152 mn higher, compared to the previous year. With the implementation of regulatory changes, the Central Bank reinforced the preventive role of bank supervision and regulated the bank restructuring process.

At the end-2015 banking system’s balance sheet assets reached BGN 87.5 bn or by 2.8% more, compared to the same period in 2014 (BGN 85.13 bn). The strong competition between banks and lower costs of borrowed funds did not manage to loosen banks’ credit policy and at the end of 2015. Thus, banks’ credit portfolio decreased 2.6% to BGN 54.1 bn, representing 61.8% of the system’s total assets.

Data published recently in the Commercial Register shows that five banks (under six years earlier) voted a total of 566 million. Lev dividends. This is 18% more than in 2014.

The contraction in loans is going on, for the eighteenth consecutive month, as of April 2016. Within the general trend, the decline of loans to non-financial enterprises was 2.2% yoy, while those to households decreased by only 1.4% yoy.

The share of non-performing and restructured loans (excluding overdrafts), however, remained at 22.6% for April, which is by 1.8pp lower yoy. Out of them the NPLs to households were 17.2%, while those to non-financial enterprises reached a more significant share of 26.9% in April. The average interest rates on new loans remained at relatively high level 6.4% yoy.

Otherwise, deposits marked an increase again by 8.0% yoy. The rise in the deposits of households’ segment reached 6.4% yoy, while the increase in the deposits of non-financial enterprises was 12.2% yoy. The average interest rate on deposits was 0.8%, following a smooth downward trend.

Low interest rates are expected to encourage household consumption in 2016, while investments, tending mostly to relay on subsidized EU financing, might step up just marginally within the ongoing resource intensive Asset Quality Review (AQR) testing in the banking sector.

Governing the sector, the BNB implemented a series of regulatory and organizational changes. New governor was voted in, before the expiration of the mandate of his predecessor, the preventive role of bank supervision was reinforced and bank restructuring process regulated. In this respect, the Bank Recovery and Resolution Directive came into effect, leading to amendments in the Law on Credit Institutions and the adoption of entirely new Law on Deposit Insurance in Banks. A Law on Recovery and Resolution of Banks and Financial Intermediaries was passed, which required the establishment of a new fund for rescuing viable institutions and implemented structural changes in the Central Bank.

In 2016 as well the banking community is working in a testing environment, as AQR will be carried out in the Bulgarian financial system, which is expected to strengthen the trust in the sector and encourage the consolidation process. Such trend was also observed in 2015, when Eurobank Bulgaria closed a deal for the acquisition of the branch network of Alpha Bank Bulgarian Branch. Meanwhile, as soon as the first quarter, the negative interest rates on excess reserves in BNB, introduced in the beginning of the year, are expected to reflect in near zero interest rates on deposits. The cleaning up of bank balance sheets will help to create the conditions for better access to finance. Clearly, banks have made substantial progress in adjusting their balance sheets and most banking institutions are well capitalised and liquid. However, the banking sector is still recording a high share of non-performing loans and bad assets.[7]

8. Conclusions

Pro-European and pro-Atlantic government coalition was voted in November 2014. It inherited a grave budget deficit, frozen EU programs and revoked license of Corporate Commercial Bank. Despite the unusual large coalition amidst low coalition culture in the country the stays in power, since people and parties are currently not convinced in the benefits of new elections, not believing that anything substantial is going to change. The low energy prices, the weak euro, the cheaper money, and the accelerated recovery of the Eurozone stimulated the real GDP growth, which increased by 3.0% in 2015 and in Q1 2016, significantly improving the result from 2014 (1.5%). Bolstered by the macroeconomic environment, the banking sector succeeded in strengthening confidence after the failure of Corporate Commercial Bank, the fourth largest lender at the time. In turn, the financial crisis in Greece had only a limited impact over the banking industry, not leading to systematic shocks. In fact, banks managed to accumulate higher liquidity and capital buffers. After 2014, 2015 has also developed as a year of deflation. This trend reflects the ongoing ECB’s QE policy and the most likely development of the electricity prices. They are envisaged to be raised, due to the huge deficits in the energy sector. Reflecting the positive dynamics of the GDP in Q1 2016, the employment rate rose by 0.8pp yoy to a level at 48.5%. The ongoing improvement in labor market is considered to continue at a moderate pace in this year. Internal economic environment seems to be problematic, while external environment remains highly unpredictable and with fare-reaching effects.

References

[1] European Commission: Report from the Commission to the European Parliament and the Council on the Progress in Bulgaria under the Co-operation and Verification Mechanism, Brussels, 27.01.2016

[2] European Commission: Recommendation for a COUNCIL RECOMMENDATION on the 2016 national reform programme of Bulgaria and delivering a Council opinion on the 2016 convergence programme of Bulgaria, Brussels, 18.05.2016

[3] Национален статистически институт: Инвестиционна активност в промишлеността, бизнес анкета, София, март 2016

[4] International Monetary Fund: BULGARIA 2015 ARTICLE IV CONSULTATION—STAFF REPORT, Washington, D.C., MF Country Report No. 15/119, May 2015

[5] European Commission: Country Report Bulgaria 2016 Including an In-Depth Review on the prevention and correction of macroeconomic imbalances, Brussels, 26.02.2016

[6] Национален статистически институт: Стопанска конюнктура, бизнес анкета, София юни 2016

[7] European Commission: COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE EUROPEAN COUNCIL, THE COUNCIL, THE EUROPEAN CENTRAL BANK, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE, THE COMMITTEE OF THE REGIONS AND THE EUROPEAN INVESTMENT BANK 2016, European Semester: Country-specific recommendations, Brussels, 18.05.2016

[1] After eight months of discussions the Parliament approved the pension reform in July 2015, proposed by the Minister of Social Affairs. According to the proposal, the retirement age will be frozen and will renew its growth in 2016. The retirement age for women will increase by two months per year until 2029, while for men during the first two years it will step up by two months and from 2018 by one. Hence, the retirement age will increase up to 65 years for both sexes by 2037. The work time required for the eligibility for receiving full pension benefits will also gradually rise by two months per year up to 40 years for men and 37 for women in 2027. Pension contributions are envisaged also to increase by 1.0% in both 2017 and 2018. Key amendments to the Social Insurance Code are related to the option for choosing five years before pension, whether instalments for a second pension to be stored in the National Social Security Institute or in a private pension fund.

[2] Correctives contributed 1.7pp

[3] In the programming period 2014-2020 Bulgaria negotiated with the European Commission (EC) EUR 7.4 splinted in 7 operational programs (OPs). Out of them "Good Governance" and "Science and Education for Intelligent Growth" are funded with EUR 1.0 bn. OP "Good Governance" (EUR 335 mn) is an extension of the old OPs "Administrative Capacity" and "Technical Assistance". The new program will finance the administrative and judiciary reform, the e-government and e-justice. On the other hand, OP "Science and Education for Intelligent Growth" (EUR 701 mn) started for the first time. Its purpose is to support Bulgarian education by improving its quality and adjusting it to the needs of the business and the modern life.

[4] Bulgaria has returned to the markets in 2012, past a decade-long pause, and has issued in each consecutive year past the return, financing its expansionary fiscal stance.